March 11, 2026

Penetration Pricing in SaaS - How to Win Markets Without Burning Through Your Runway

Written by

Content Marketing Manager

March 11, 2026

Penetration pricing is when you deliberately set your SaaS price well below competitors to capture market share fast, and then raise prices once you’ve built retention and proven value. It’s a temporary market-entry tactic with a planned exit, not a long-term competitive position.

That distinction matters more than most founders realize. If you’re pricing low because you’re afraid to charge more, that’s underpricing, and it will quietly drain your runway without ever building the customer loyalty or market position you need. Penetration pricing, done right, is a calculated bet with a specific payoff timeline. Underpricing is just fear dressed up as strategy.

This guide covers when penetration pricing actually works, the specific conditions that have to be true, how AI is reshaping the math right now in 2026, and how to use tools like GrowthOptix to track whether your strategy is building toward something sustainable or digging a deeper hole every month. Everything here is grounded in documented research, real financials, and patterns you can verify yourself.

OpenView’s 2018 Expansion SaaS Benchmarks study (openviewpartners.com/blog/the-unspoken-impact-of-pricing-changes/) surveyed over 400 SaaS companies and found that among those who changed pricing, 98% saw a positive or neutral impact on growth. Two out of five saw a 25% or greater jump in annual recurring revenue. Companies that changed pricing grew at a 65% median rate, while companies that held pricing steady grew at 50%.

So price changes clearly work. But whether low prices work depends entirely on your unit economics. Here are the benchmarks that separate sustainable penetration pricing from a slow path to insolvency:

Aggressive movers push 15–25%. Price increases are the industry norm now, not the exception.

That last row deserves extra attention. If SaaS companies across the board are raising prices 8–12% every year, your eventual transition from low to normal pricing is not unusual. Your customers already live in a world where software gets more expensive annually, and that context should give you real confidence when it comes time to raise your own prices.

These two strategies get mixed up constantly, and the confusion can lead you into a pricing structure you never intended. Competitive pricing means you look at what others charge and price somewhere nearby. It’s an ongoing positioning exercise. Penetration pricing is fundamentally different: you’re intentionally pricing way below competitors, accepting losses, with a specific plan and timeline to raise prices later.

Here’s a practical way to tell them apart. If your competitor charges $50/month and you charge $45, that’s competitive pricing. But if you charge $15 while knowing the product is worth $50, and you have a documented plan to reach $45 within two years, that’s penetration pricing. The gap between those two scenarios is enormous in terms of capital requirements, risk, and execution complexity.

Price skimming goes the other direction entirely. You start high with early adopters who will pay a premium, then lower prices over time to reach broader markets. Apple does this with every iPhone launch. Value-based pricing sits between these approaches: you charge based on what the product is actually worth to the customer, and you adjust as you learn more about willingness to pay.

Research from Price Intelligently (now SBI Growth) found that most SaaS companies spend about six hours total on their pricing strategy (sbigrowth.com/price-intelligently). Six hours. That’s not penetration pricing or value-based pricing or any kind of deliberate pricing. So before you label what you’re doing as “penetration pricing,” it’s worth asking yourself honestly whether you chose this strategy based on research and financial modeling, or whether you defaulted to it because charging more felt scary.

Simon-Kucher’s research on pricing strategies (simon-kucher.com) gives us the clearest framework here. Their work on penetration versus skimming strategies identifies the conditions under which low-price market entry succeeds. Not every condition needs to be perfect, but if you’re missing more than one or two, a different approach will almost certainly serve you better.

This is the most important condition. Price elasticity means that when you lower your price, demand increases by a proportionally larger amount. If you drop your price 20% and demand jumps 40%, that’s elastic demand, and the volume more than compensates for the thinner margin. But if you drop 20% and demand only ticks up 10%, you’ve just destroyed revenue for a negligible gain.

Most companies don’t know their price elasticity before launch. You’re guessing. One way to reduce that guessing is the Van Westendorp Price Sensitivity Meter, which asks your target customers four questions: at what price would you doubt the quality, at what price does it feel like a bargain, when does it start feeling expensive, and when is it too expensive to consider. The overlap between those answers gives you a real range to work with, and it takes the gut-feel out of a decision that deserves hard data.

Slack gets more useful when your whole team is on it. Zoom becomes the default when everyone has it installed. Every new user you acquire through low pricing makes the product stickier for everyone else. That kind of network effect is the best advantage a penetration pricing strategy can have, because each new customer doesn’t just generate revenue, they make the product harder to leave for every other customer.

Traditional SaaS also benefits from near-zero marginal costs. Adding one more customer to your platform costs almost nothing, so high volume at lower prices can still work economically.

But here’s the 2026 reality that changes this calculation. If your product runs on AI inference, your marginal costs are real and significant. OpenAI’s gross margins sit around 33–40%, well below the 60–80% range for traditional SaaS. Every customer interaction costs actual compute money. So if you’re building an AI-native product and trying to do penetration pricing at the same time, you’re compressing margins from two directions, and that’s a much harder game to win.

This condition is where most penetration attempts fail. If the only reason someone buys your product is because it’s cheap, you have no defense when a competitor matches your price or undercuts you.

When Freshworks launched against Zendesk, the low price got people in the door, but the product experience is what kept them there through subsequent price increases. Intercom’s Fin AI agent charges just $0.99 per resolution, and that works because the product actually resolves customer issues autonomously. In both cases, the price serves as the hook, but the product itself is the anchor. Without that anchor, you’re competing on cheapness alone, and that’s a position you can’t defend.

Penetration pricing means losing money on purpose. You need enough capital to survive the loss period and come out the other side with a customer base that justifies the investment. Here’s how that timeline typically breaks down:

You’re raising prices, approaching breakeven, and testing what the market will bear.

If you only have twelve months of runway and try aggressive penetration pricing, you’ll probably run out of money somewhere in phase two. That’s not a pricing strategy. That’s a countdown clock with no plan for what happens when it reaches zero.

The math here is straightforward. If you’re charging $9/month instead of $29/month, you need roughly three times as many customers to hit the same revenue. Penetration pricing works when you’re going after millions of potential users, not a few thousand in a narrow vertical.

In micro niches, customers tend to stay with their existing tools for years. They care about functionality, support, and reliability. A lower price won’t pull them away from something they trust, and even if it did, the total addressable market just isn’t large enough to make the volume economics work.

Knowing when to walk away from this strategy is just as important as knowing when to use it. If any of these sound like your situation, penetration pricing will likely hurt more than it helps.

Your minimum viable annual revenue per customer comes down to math, not gut feeling. Here’s the formula:

Say your CAC is $5,000, it costs you $500/year to serve each customer, and you’re targeting a 75% gross margin. Your minimum viable ARPU works out to ($5,000 + $500) / (1 - 0.75) = $22,000/year.

Now compare that to your actual pricing. If you’re charging $750/month ($9,000/year) against a $22,000 minimum, you’re subsidizing nearly 60% of your required revenue per customer with investor money. That subsidy might make sense temporarily if you meet all five criteria above, but you need to know exactly when it ends. Have you set a specific revenue milestone that triggers your pricing transition, or are you telling yourself you’ll figure it out later? That honest answer separates founders running a strategy from founders running on hope.

Frameworks and formulas are useful, but nothing teaches like real examples. These three companies each took a different path with penetration pricing, and their outcomes show exactly why the conditions above matter so much.

OpenAI is the biggest penetration pricing bet happening in tech right now. ChatGPT launched with free access and a $20/month paid tier for a product worth far more than that, and the approach produced the fastest-growing user base in history, reaching 200 million weekly active users (theverge.com/2024/8/29/24231685/openai-chatgpt-200-million-weekly-users).

The cost of that growth is staggering. In 2024, OpenAI lost roughly $5 billion on $3.7 billion in revenue (cnbc.com/2024/09/27/openai-sees-5-billion-loss-this-year-on-3point7-billion-in-revenue). Revenue tripled to $13.1 billion in 2025, but cumulative losses are projected at $14 billion by 2026 (the-decoder.com/openai-adds-111-billion-to-its-cash-burn-forecast-as-ai-costs-spiral-beyond-projections/). Gross margins sit around 33–40% because inference compute costs quadrupled in a single year. The company doesn’t expect to reach positive cash flow until 2030.

OpenAI can sustain this because they raised over $40 billion in a single funding round from SoftBank, they have Microsoft as a strategic backer, and they’ve built a product so deeply embedded in daily workflows that switching costs are enormous. The lesson here isn’t to lose billions. The lesson is that penetration pricing at this depth requires capital that matches the depth of the losses, combined with product stickiness that prevents churn when prices eventually rise. If you can’t match both of those conditions, the OpenAI playbook won’t translate to your business.

Slack reached $100 million in annual recurring revenue in just two and a half years, which at the time was the fastest any SaaS company had achieved that milestone (medium.com/startup-grind/growing-as-fast-as-slack-195c1e194561). They did it with a generous free tier that included message history limits, paired with low-friction per-seat paid plans.

The free tier functioned like penetration pricing because once a team’s conversations lived in Slack, switching became genuinely painful. The network effect did the heavy lifting. People didn’t upgrade because Slack pushed a price increase on them. They upgraded because their team outgrew the free tier and the product had become too essential to walk away from. That’s the ideal version of how penetration pricing is supposed to play out: the low price brings people in, and the product makes them stay through the transition to higher prices.

Artisan, an AI outbound sales platform, launched with product-led growth and very cheap pricing. Tina Sang, the company’s Chief of Staff, described what happened in an interview published on ChartMogul’s blog (chartmogul.com/blog/penetration-pricing-in-saas/): hundreds of users signed up quickly, but most of them were early-stage startups that hadn’t found product-market fit. Those users didn’t get results on the platform, and they churned out almost as fast as they came in.

Artisan pivoted to a sales-led model with higher prices and custom contracts. That’s when things turned around, and the company grew to $2 million in ARR by attracting customers who were serious enough to pay for real value.

This is worth thinking about carefully for your own business. Are you attracting customers who will actually succeed with your product and stay through a pricing transition? Or are you pulling in bargain hunters who will leave the moment something cheaper shows up? The customers you attract at penetration prices are the customers you’ll need to retain at normal prices, so the quality of those early cohorts determines whether the entire strategy works.

The wrong customer problem. Low prices attract price-sensitive buyers who tend to churn when prices go up, generate less expansion revenue, cost more in support relative to what they pay, and switch the moment a competitor undercuts you. You end up filling a leaky bucket. Customers pour in the top and drain out the bottom, and you never build the stable base that justifies your early losses. Artisan’s story above shows exactly how this plays out in practice.

The transition trap. You’ve built your entire customer base around low prices. Now you need to raise them. Some customers churn. Some feel baited and switched. New prospects see existing users paying less and wonder why they should pay more. Bubble, the no-code platform, went through this publicly. After a price increase, users organized on Reddit and many switched to cheaper alternatives. If an established brand like Bubble struggles with pricing backlash, companies without that level of loyalty should expect even more resistance.

The competitive response. When you launch cheap, competitors notice. If they have deeper pockets, they match your price and outlast you. If they’re smart, they frame your low price as a sign of inferior quality, or they bundle extra features at their existing price point. They might also target segments where price isn’t the deciding factor. If you can’t differentiate beyond price, you’ve started a fight that you may not have the resources to finish.

Most founders put off their transition plan until they’re running low on cash. That’s the worst possible time to make pricing decisions, because urgency leads to rushed changes, and rushed changes lead to churn. Your transition plan should exist before you launch at a low price.

The OpenView data is genuinely reassuring here (openviewpartners.com/blog/the-unspoken-impact-of-pricing-changes/). Among companies that changed pricing, 98% saw positive or neutral outcomes. The small minority that experienced negative impact typically violated multiple implementation principles at once: no advance notice, no value justification, no consideration for existing customers. When you do it right, price increases work. Here’s what “right” looks like in practice:

For the timeline, a graduated approach works best. Year one, keep penetration pricing but focus on reducing time-to-value and documenting ROI you can point to later. Year two, introduce premium tiers for new customers without forcing changes on existing ones. Year three, raise prices 15–20% for new customers, which is well within current industry norms. Year four, transition grandfathered customers with visible product improvements that justify the new pricing.

Throughout this entire process, pay close attention to whether your penetration-priced customers are expanding or just sitting at the minimum. If they’re adding seats, upgrading features, and increasing usage, your transition will go smoothly. If they’re static, you may have a customer quality problem that no amount of careful communication can fix.

The SaaS pricing landscape is going through its most disruptive shift since the move from on-premise to cloud. These changes are happening right now, and they directly affect whether penetration pricing makes sense for your product today.

AI agents are reducing how many human users organizations actually need, which undermines the per-seat pricing model that most SaaS companies depend on. In early 2026, this dynamic contributed to roughly $285 billion in market cap losses across the software sector (intellectia.ai/blog/will-ai-disrupt-saas-business-model-2026) in what people are calling the SaaSpocalypse. Companies aren’t struggling because AI failed. They’re struggling because AI succeeded, and their customers are cutting seats as a result.

If you’re pricing low per seat and your customers are also reducing seats because of AI, your revenue per account shrinks from two directions at once. That’s a compounding problem, and you need to model it carefully before committing to a per-seat penetration strategy in the current environment.

A fundamentally different pricing model has emerged where companies charge for results delivered rather than access provided. Here’s what that looks like in practice right now:

Outcome-based pricing is worth serious consideration because it can eliminate several of the biggest risks of penetration pricing entirely. Customers start at zero cost and scale up as the product delivers results. You never have to plan a painful transition to higher prices. The wrong customer problem largely disappears, because people who don’t get value don’t pay, and people who get significant value pay accordingly. Gartner projects that by 2030, at least 40% of enterprise SaaS spend will shift toward usage-based, agent-based, or outcome-based pricing (deloitte.com/us/en/insights/industry/technology/technology-media-and-telecom-predictions/2026/saas-ai-agents.html), and that shift is well underway today.

Some vendors are now pricing AI agents at $800 to $2,000+ per month, positioning them as full-time employee replacements rather than software tools. The cost anchor shifts from a $20/month software license to a $60,000 annual salary, which allows for dramatically higher contract values.

If your AI product replaces a human role, pricing it cheaply can actually backfire. Buyers expect to pay something closer to the labor equivalent, and an artificially low price triggers doubt about whether the product can really do the job. In this context, penetration pricing doesn’t just leave money on the table. It actively undermines the trust you’re trying to build with your buyer.

Companies like Notion, Slack, and Loom initially charged $4–10 per user for an AI add-on and have since bundled AI into their core product while raising base prices by $2.50–$5 per user. HubSpot uses a credit model where core plans include a bank of credits that reset monthly, with additional credits available for purchase.

For your penetration pricing strategy, this means the traditional model of offering low flat-rate access and raising prices later is getting more complicated. The market is simultaneously experimenting with credits, usage tiers, and outcome-based components. You need to think about which pricing model you’ll eventually transition to, because that model may not be a simple per-seat increase anymore.

Penetration pricing plays out very differently depending on where you’re selling. In markets like Latin America, you might face two or three competitors instead of fifteen. That lower competitive density means your low pricing won’t immediately trigger a destructive price war the way it often does in the US market.

But regional pricing adjustments and penetration pricing are two different things. Major SaaS companies like Spotify and Netflix adjust pricing across regions based on purchasing power. If you’re entering a new market, consider whether you actually need a penetration strategy or just a price that reflects local economic realities. And regardless of which approach you choose, payment method accessibility matters enormously. If your target customers can’t easily pay you with the methods available in their market, your pricing strategy becomes irrelevant.

The difference between founders who succeed with penetration pricing and those who slowly bleed out comes down to measurement. Not annual reviews or quarterly check-ins, but ongoing visibility into whether your low prices are building toward something sustainable or just postponing a reckoning.

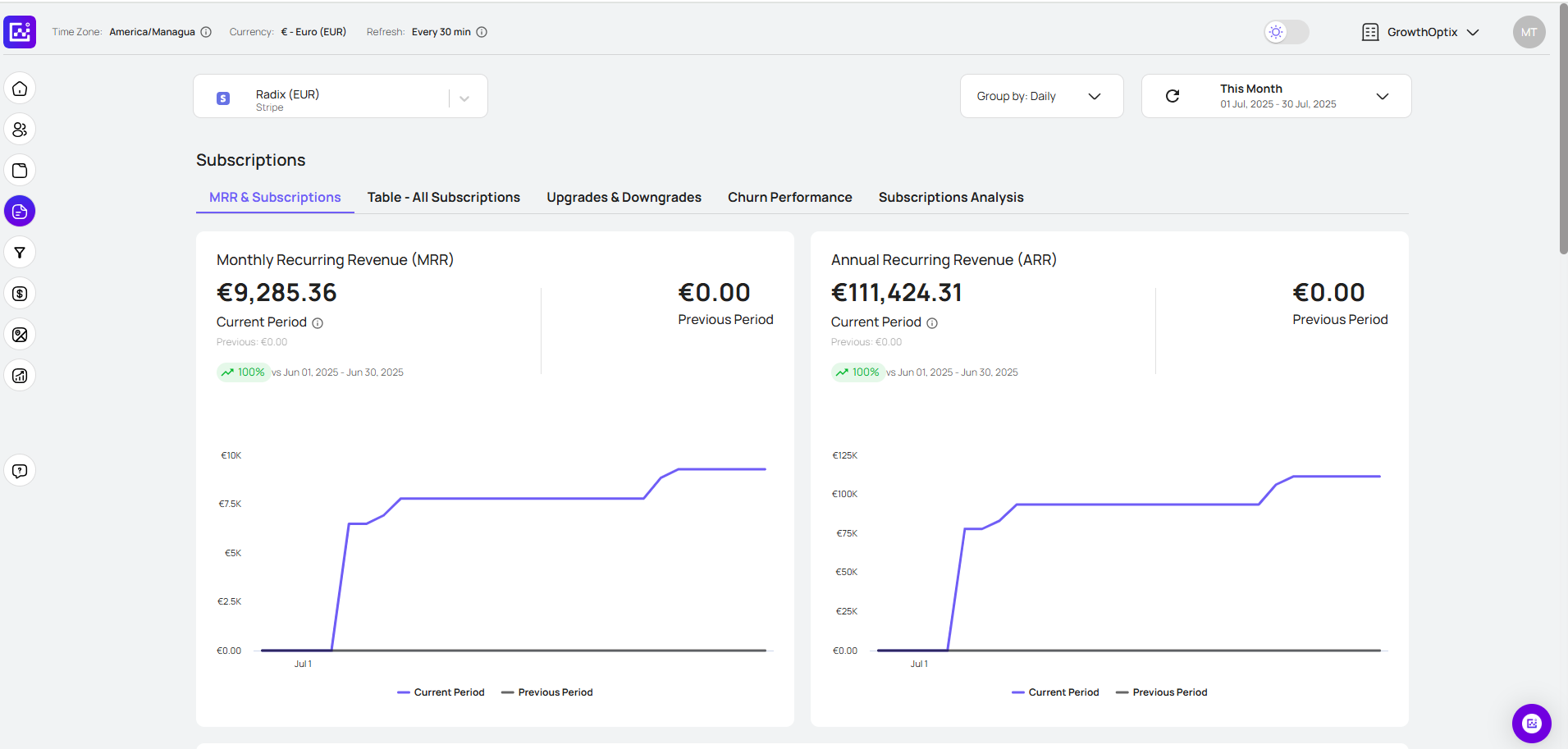

GrowthOptix gives you that visibility. Here’s what that looks like in practice.

Set data-driven pricing transition triggers. Instead of waiting until cash gets tight and scrambling to raise prices, use GrowthOptix’s MRR tracking to define specific revenue milestones that signal when you’re ready to move. Tie those milestones to your ARPU formula and CAC payback targets. When you hit them, you have an objective basis for raising prices, which is far more reliable than a gut feeling or a board member’s opinion.

Compare retention across pricing cohorts. The wrong customer problem is only detectable through cohort analysis. GrowthOptix lets you compare retention and expansion metrics between customers acquired at penetration prices and those at standard pricing. If your cheap cohorts churn faster, adopt fewer features, and generate less expansion revenue, you’re watching the leaky bucket form in real time. That early signal gives you the chance to adjust course before the problem becomes structural.

Monitor net dollar retention by pricing segment. NDR is the single most important diagnostic for whether your penetration strategy will survive the transition to higher prices. GrowthOptix lets you segment NDR by pricing cohort, so you can see whether your penetration-priced customers are expanding through additional seats, feature upgrades, and increased usage, or whether they’re sitting at the minimum and contributing nothing beyond their initial low payment. That distinction determines everything about your transition readiness.

Track LTV:CAC by acquisition price point. The 3:1 ratio is a benchmark for your overall business, but you need to know whether your penetration-priced customers specifically are on track to reach it. GrowthOptix breaks this down by how customers were acquired and what they’re paying, turning an abstract industry benchmark into a diagnostic tool you can act on this month.

If your situation doesn’t match the five criteria, these alternatives are often the smarter path. Each one addresses a different set of constraints:

Products with viral adoption, network effects, and addressable markets large enough that 95%+ free users are sustainable.

Usage-based pricing deserves particular attention because it gives you a penetration-like entry point without the transition problem. Customers start small and cheap, then expand organically as usage grows. You never have to implement a jarring price increase because the price scales with value naturally. Twilio, Stripe, and Snowflake all built massive businesses this way, and the model is especially well-suited to the current SaaS environment where buyers want pricing that reflects what they actually use.

Run through these questions honestly. Not the answers you wish were true, but the ones that actually reflect where your business stands today.

Market: Is your addressable market measured in millions? Do you have network effects or viral mechanics that make each new customer more valuable to existing ones? Are incumbents overpriced relative to the value they actually deliver?

Product: Is your product differentiated beyond price? Can users reach meaningful value within the first week? Do you have natural expansion paths like additional seats, features, or usage tiers that drive revenue growth within existing accounts?

Financial: Do you have 18+ months of runway to sustain losses? Can you keep gross margins above 60% even at low prices? Will your LTV:CAC ratio reach 3:1 within a realistic timeframe given your current acquisition costs?

Execution: Do you have customer success infrastructure to prove ROI? Have you tested whether demand actually increases meaningfully when you lower price? Do you have a specific, time-bound plan for price increases with defined triggers and a communication strategy?

If you’re saying yes to most of these, penetration pricing could work for you. If you’re saying no to half or more, one of the alternatives in the table above will almost certainly serve you better. And if you’re unsure about some of the financial answers, that’s exactly where GrowthOptix helps. Set up your cohort tracking and MRR dashboards before you commit to a pricing strategy, so you’re making the decision with data rather than assumptions.

Penetration pricing is generally considered ethical when your prices cover costs and you’re not trying to eliminate competition through predatory practices. Selling below cost specifically to push competitors out of a market can raise antitrust concerns in certain jurisdictions. For most SaaS companies this isn’t a practical issue since the goal is market entry, not competitor destruction. But if your strategy involves sustained below-cost pricing with the specific intent of driving others out of business, it’s worth a conversation with legal counsel.

Be honest about whether you chose this strategy or defaulted to it. Strategic penetration pricing has a documented plan, specific metrics, defined transition triggers, and a timeline. Underpricing has a vague justification and a hope that growth will somehow sort things out. Take a hard look at which one you’re actually running.

Price increases work when you do them right. The data shows 98% positive or neutral outcomes across hundreds of companies. Advance notice, value justification, grandfather periods, and transparent communication are what make the difference. If the eventual price increase is what’s holding you back from this strategy, the evidence should put that concern to rest.

Three years is too long to stay at penetration prices. If you’re still pricing low after three years, either you failed to execute the transition or you never had a real penetration strategy to begin with. Both scenarios typically mean unsustainable unit economics that are holding back your growth right now.

AI is changing the math today, not someday. Outcome-based and usage-based pricing may eliminate the need for penetration pricing entirely for AI-native products. Before defaulting to “price low now, raise later,” seriously evaluate whether a model that ties price to value from day one would work better for what you’re building.

Measurement is what separates strategy from guesswork. Track MRR by pricing cohort. Compare NDR across customer segments. Monitor LTV:CAC by acquisition price point. Set specific triggers for transitions. GrowthOptix makes this level of granularity accessible so you’re making pricing decisions based on what’s actually happening in your business, not on anxiety or outdated spreadsheets.

If you haven’t launched yet, resist the temptation to default to penetration pricing because it feels safer. Run through the decision framework above. If you don’t clearly meet most of the criteria, start with value-based, usage-based, or outcome-based pricing instead.

If you’re already using penetration pricing, build your transition plan today. Define the metrics that trigger price increases. Write the customer communication plan. Set up cohort tracking in GrowthOptix so you can see in real time whether your penetration-priced customers are building toward sustainability or creating a problem you’ll have to solve under pressure later.

If your competitors are using penetration pricing, don’t automatically match them. Focus on what makes your product different: better customer success, stronger targeting in specific segments, capabilities they can’t replicate. Let them burn capital while you build economics that actually sustain growth.

The goal was never to implement penetration pricing. The goal is to build a company with sustainable revenue, healthy margins, and a customer base that grows in value over time. Choose the pricing strategy that serves that goal, measure its impact rigorously with the right tools, and be willing to evolve your approach as the market shifts around you. In 2026, it’s shifting fast.

Join hundreds of SaaS companies who finally understand which marketing drives profitable growth.